Formynder Blog

Featured

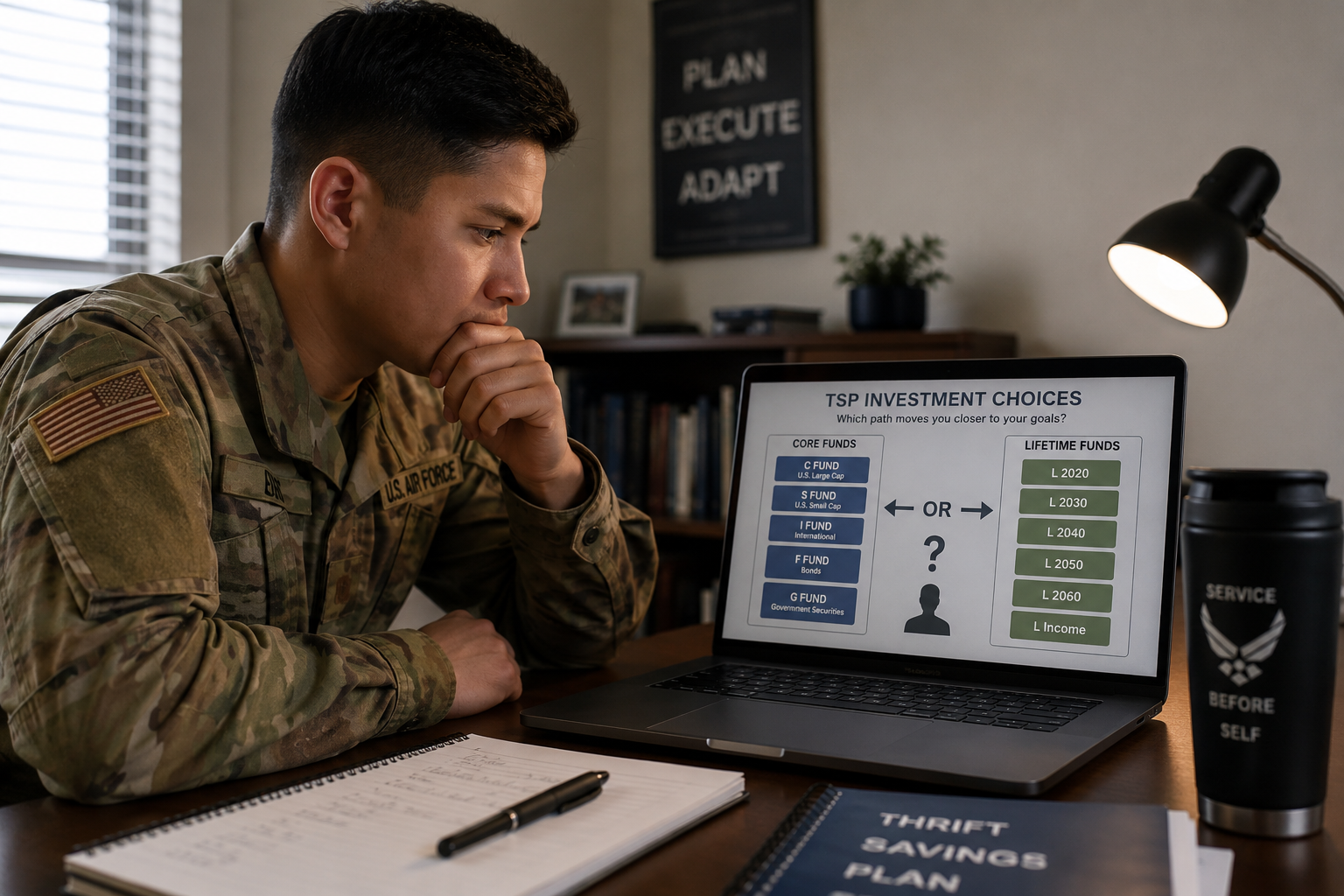

G, F, C, S, I, L 2050. TSP fund names can feel like a foreign language sometimes. Here's what each one actually does, why the default Lifecycle Fund may not fit a military retirement timeline, and why mixing core funds with an L Fund often backfires.

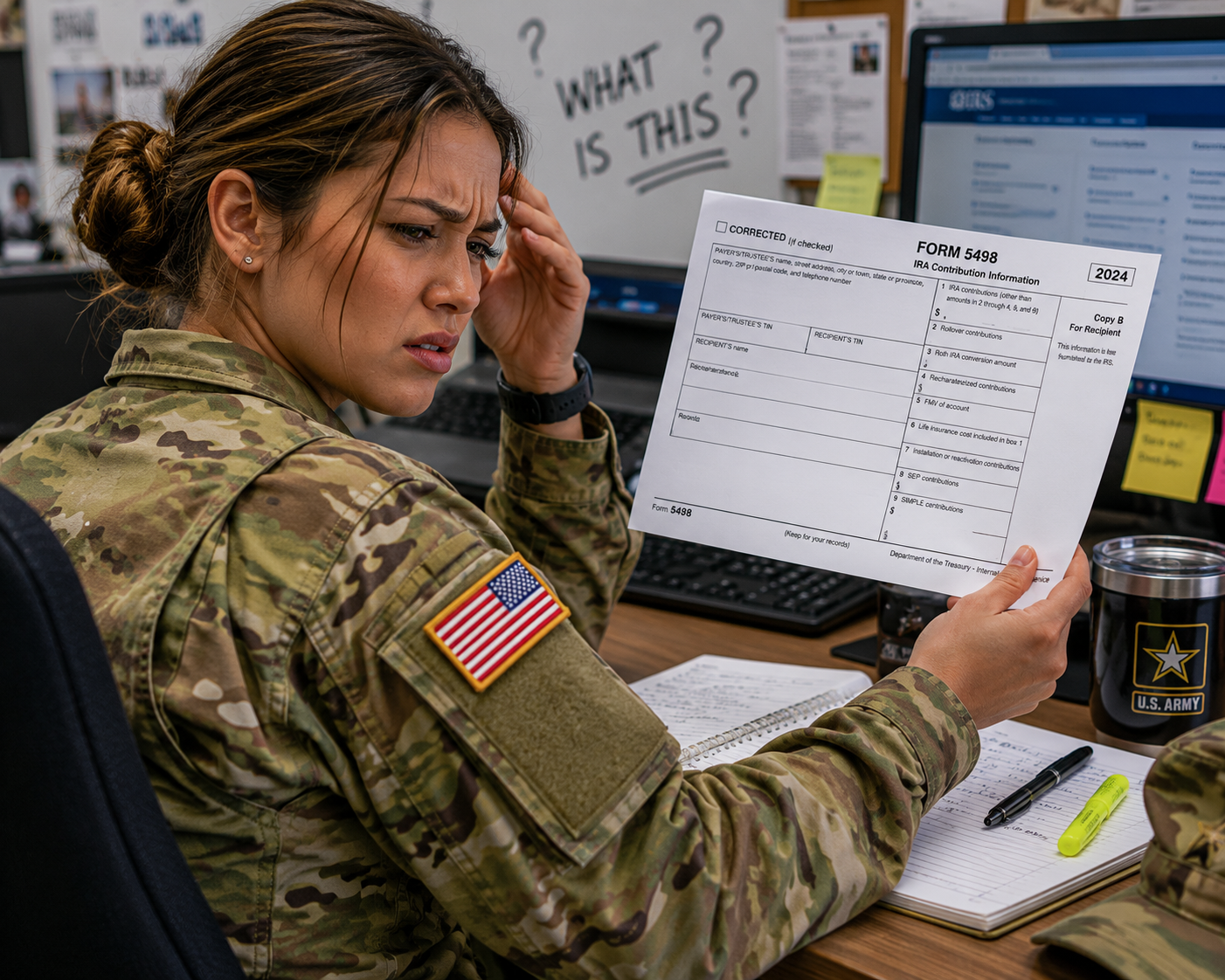

Every May, a form arrives from an IRA custodian. Tax season is over, the return is filed, and now there is a piece of IRS paperwork sitting on the counter. That form is 5498, and despite the timing, nothing went wrong. But ignoring it has a way of creating expensive problems down the road.

What does year one of building a financial planning firm actually look like? Not the version you post on LinkedIn -- the real one. Mine started with an inbox ping at a breakfast table in the middle of MilMoneyCon and ended with more client households than I originally targeted, a fee model I actually believe in, and more self-awareness than I expected to gain in twelve months. Along the way there were slow months, steering away from “the way it’s always been done”, people who showed up in ways I didn't see coming, and more than a few things I am still figuring out. Curious? Keep reading.

In a combined arms operation, the mission succeeds not because one element outperforms the others, but because every element knows its role and coordinates toward a common objective. No single asset wins the engagement alone. The same principle applies to building a financial team for military life. The right professionals, working in their own lanes and communicating across them, give military families the structure to identify meaningful goals, aim their resources effectively, and execute a plan that holds together across every stage of service and beyond.

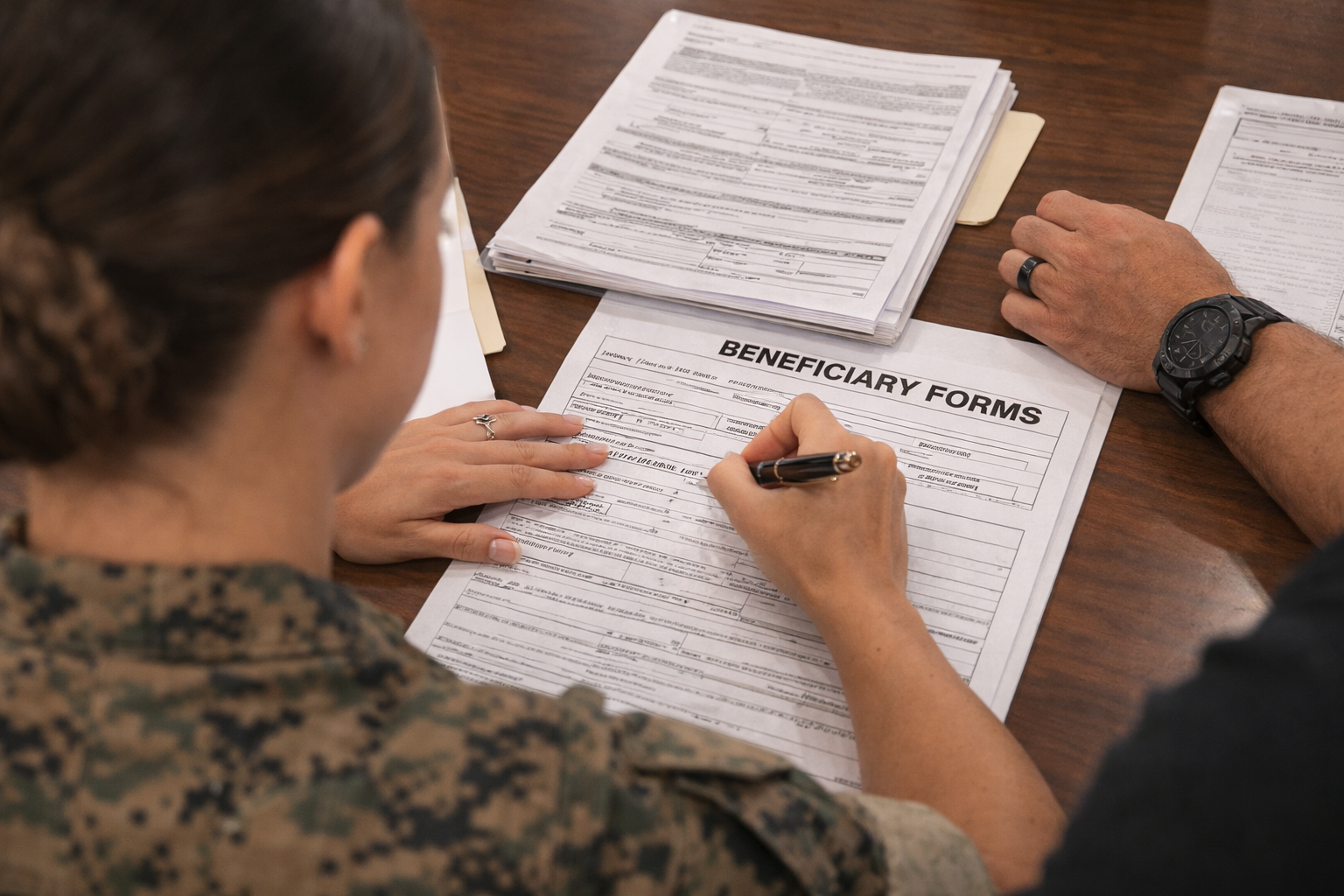

Estate planning is not just about what happens when you pass. It is also about who makes decisions if you cannot, who cares for your children in a gap between an emergency and a family member's arrival, and whether the right people have the authority to act when it matters most. For military families navigating PCS moves, deployments, and duty stations far from home, those questions carry real weight. This article defines the core estate planning documents every military family should understand, and explains what makes them work differently in a military life than they do for everyone else.

Estate planning has a reputation for being the financial task everyone intends to do and very few actually get around to. For most military members, there is really only one moment that forces the conversation: pre-deployment workups. But life changes far more often than a deployment cycle, and very few of those changes trigger a follow-up review of the financial accounts that matter most.

TRICARE covers the medical side of military healthcare, but dental and vision are a different story. For military retirees and active-duty families, the Federal Employees Dental and Vision Insurance Program (FEDVIP) fills that gap with voluntary, competitively priced coverage. Understanding who qualifies, what it covers, and whether the premiums make sense for your family is worth a closer look before the next open season arrives.

You spent decades earning your military retirement benefits. At 65, one of the most valuable pieces of that package clicks into place: TRICARE for Life alongside Medicare. But enrollment windows are unforgiving, the overseas rules surprise most retirees, and something called IRMAA can inflate your Medicare premiums for years if income is not planned carefully. Here is everything you need to know before that birthday arrives.

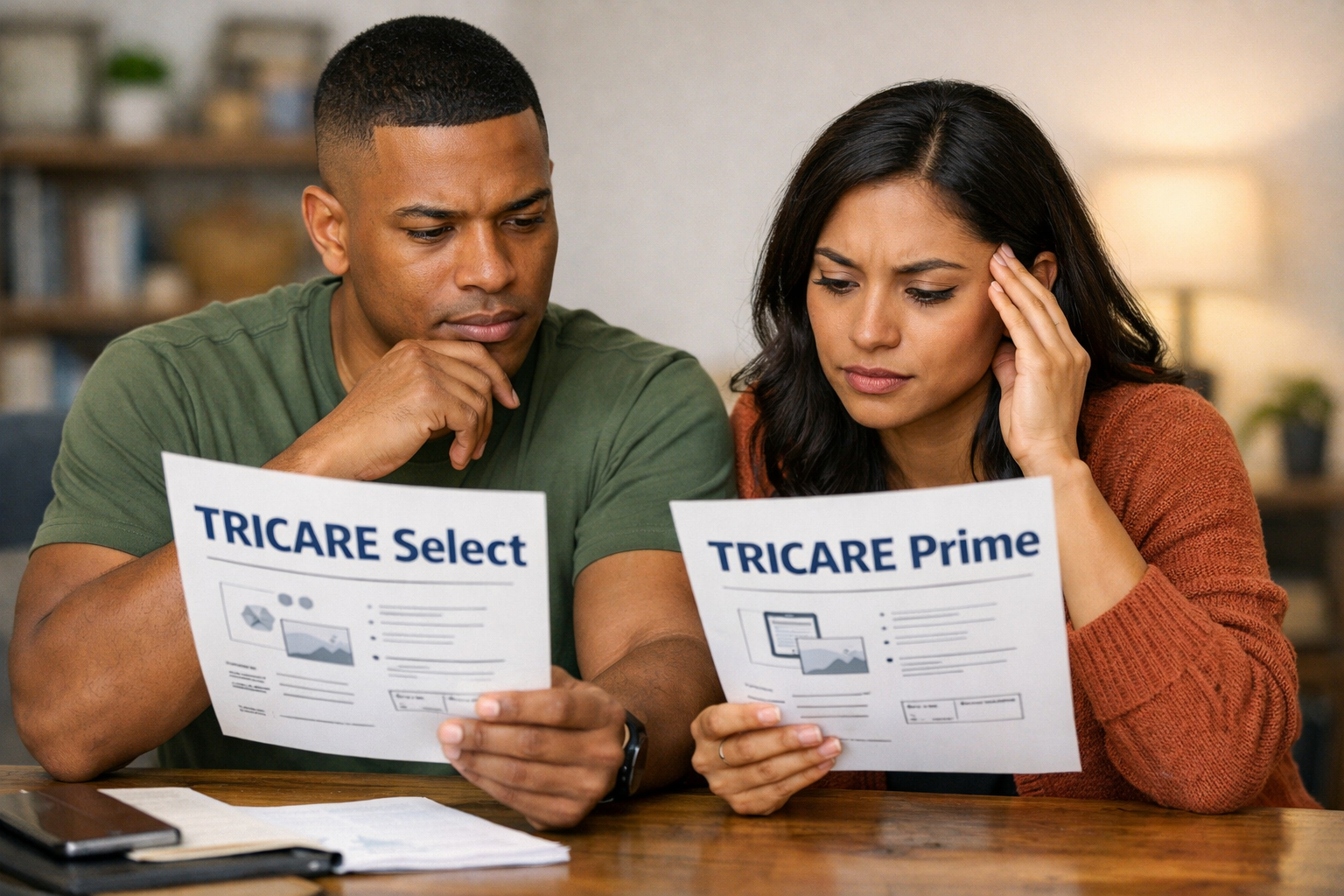

Comparing TRICARE Prime and TRICARE Select as a military retiree? This guide breaks down provider choice, enrollment fees, deductibles, copays, and catastrophic caps so you can make a confident decision for you and your family.

Homeowners insurance is more than a closing requirement. For military families who move frequently and invest in homes across different markets, Coverage A and rebuild cost play a critical role in long-term financial protection. Falling below 80% of rebuild value can lead to significant out-of-pocket costs, making an annual policy review essential.

The 50-20-20-10 rule of thumb offers a practical way for military families to think about cash flow. It helps create space for spending, saving, and giving while keeping mandatory expenses under control. More than anything, it serves as a conversation starter within households, helping couples stay aligned on financial priorities and avoid the stress that often comes when money begins to drift out of balance.

Generosity has always been a core part of Christian stewardship, but it also plays an important role in a healthy financial plan. For military families, intentional giving can align financial decisions with the values of service, faith, and community. By incorporating generosity into a structured framework, families can plan their spending, saving, and giving in a way that supports both financial stability and meaningful impact.

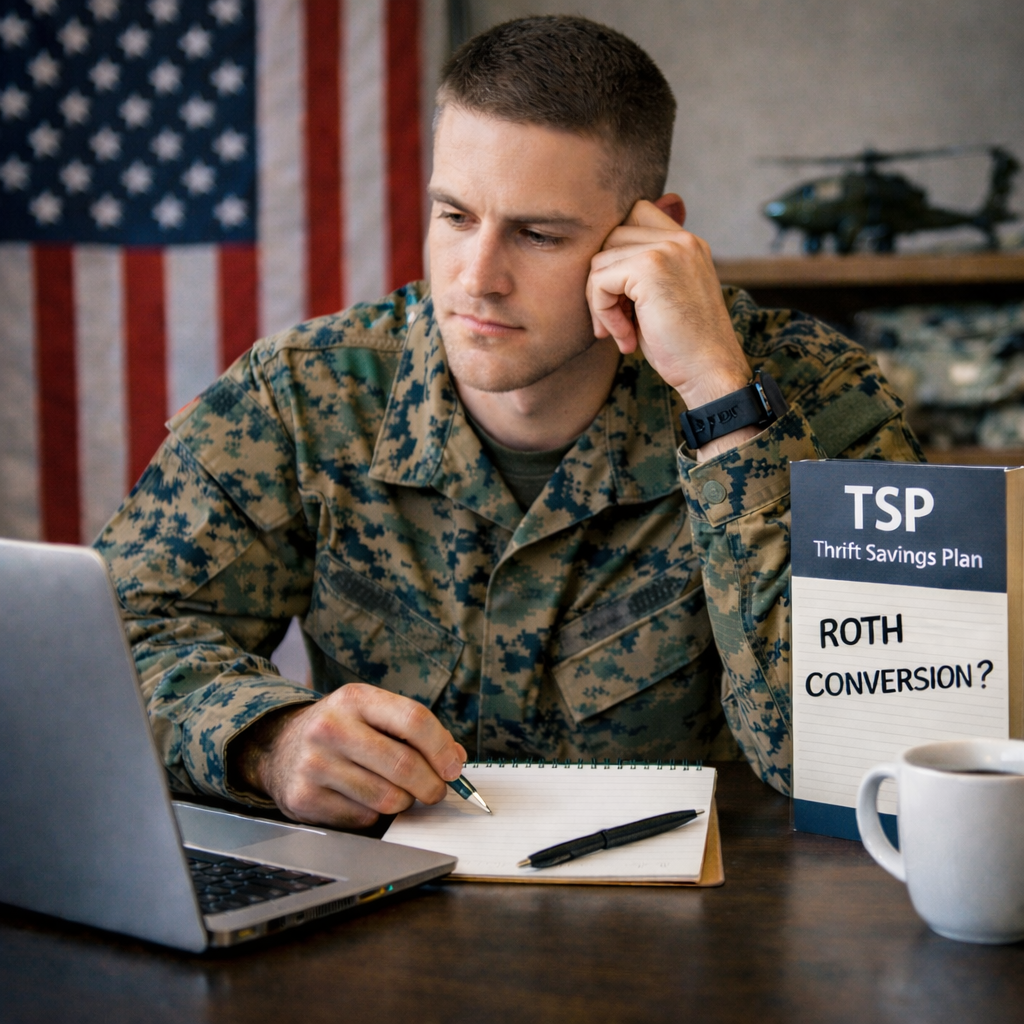

A Roth conversion inside the TSP can be a powerful tax move for military members and federal employees. It can also be an expensive mistake. The recent addition of TSP in-plan Roth conversions gives you more control over when you pay taxes, but it also adds complexity that many participants overlook. Whether you're active duty, transitioning, or already retired, understanding how conversions affect your tax bracket, pensions, future RMDs, and overall retirement strategy is critical. This article breaks down what an in-plan Roth conversion really does, who it tends to benefit, and the specific TSP rules you need to know before making a permanent decision.

Military retirement changes how investment risk should be evaluated. A military pension and VA disability income provide guaranteed, inflation-adjusted lifetime income that can significantly reduce reliance on an investment portfolio for mandatory expenses. This shift directly impacts asset allocation, retirement glide path decisions, and overall risk capacity. Unlike civilian retirees who depend heavily on 401(k) or IRA withdrawals, military retirees whose pension covers core living expenses may have greater flexibility to maintain higher equity exposure for long-term growth. Understanding your risk need, or how much your investments must generate to fund your lifestyle, is critical when designing a military retirement investment strategy.

Tax season often feels simple until it suddenly isn’t. One year it is a straightforward W-2 and standard deduction. The next, you are navigating rental properties in multiple states, Roth conversions, IRA deductibility questions, or a major income increase from promotion or transition. For military families building wealth, tax complexity can escalate quickly. This article outlines five clear signs it may be time to seek professional tax help, before April arrives and planning opportunities have already passed.

Military parents already juggle enough financial complexity without adding another confusing savings vehicle to the mix. Trump accounts are a new, government-created option for children that come with a headline benefit; a potential $1,000 seed deposit for eligible kids. They also strict rules, limited flexibility, and long-term tradeoffs. Before opening one, families should step back and ask a simple question: what are you actually saving for? This guide breaks down how Trump accounts work, who qualifies, and why they are rarely the automatic choice compared to more established options like 529 plans or Roth IRAs.

On July 4th, President Trump signed the One, Big, Beautiful Bill (OBBB) into law, ushering in a wave of tax changes with immediate and long-term implications. While the full bill is extensive, this article distills the most relevant provisions for military families, highlighting what may impact your 2025 tax return and future financial planning.

Gambling is no longer limited to casinos or occasional poker nights. Today, betting apps place wagering in a service member’s pocket; available 24/7, private, and frictionless. For military personnel, the consequences can extend far beyond lost money. Gambling-related financial stress can threaten security clearances, disrupt steady pay, strain family relationships, and impact long-term career readiness. Understanding these risks is essential for protecting both financial stability and military service.

This article offers an educational perspective on the Survivor Benefit Plan (SBP) that goes beyond rates of return and spreadsheet comparisons. It is intended to help military families reframe the SBP decision as a question of survivor income, emotional burden, and long-term peace of mind, particularly for the spouse who would live with the outcome. The discussion is general in nature and meant to encourage thoughtful conversation between partners.

If your military pension or VA disability covers your core expenses, your emergency fund may need a rethink. Learn how to right-size it with confidence.

Many military families are targeted by salespeople posing as financial advisors. These individuals often promote complex insurance products, such as whole life or indexed universal life (IUL) policies, as “wealth-building” strategies.

This article examines how one such case exposed the dangers of commission-driven advice and highlights practical ways to identify the difference between a true fiduciary and a salesperson in disguise. It also provides key questions to ask, resources to verify credentials, and guidance on how to find professionals who act in your best interest.

Leaving the military comes with a long list of decisions, and your Thrift Savings Plan (TSP) is one of them. Should you keep it, roll it into an IRA, or move it into a new employer plan? This article breaks down the pros and cons of each choice so you can approach your retirement transition with clarity and confidence.

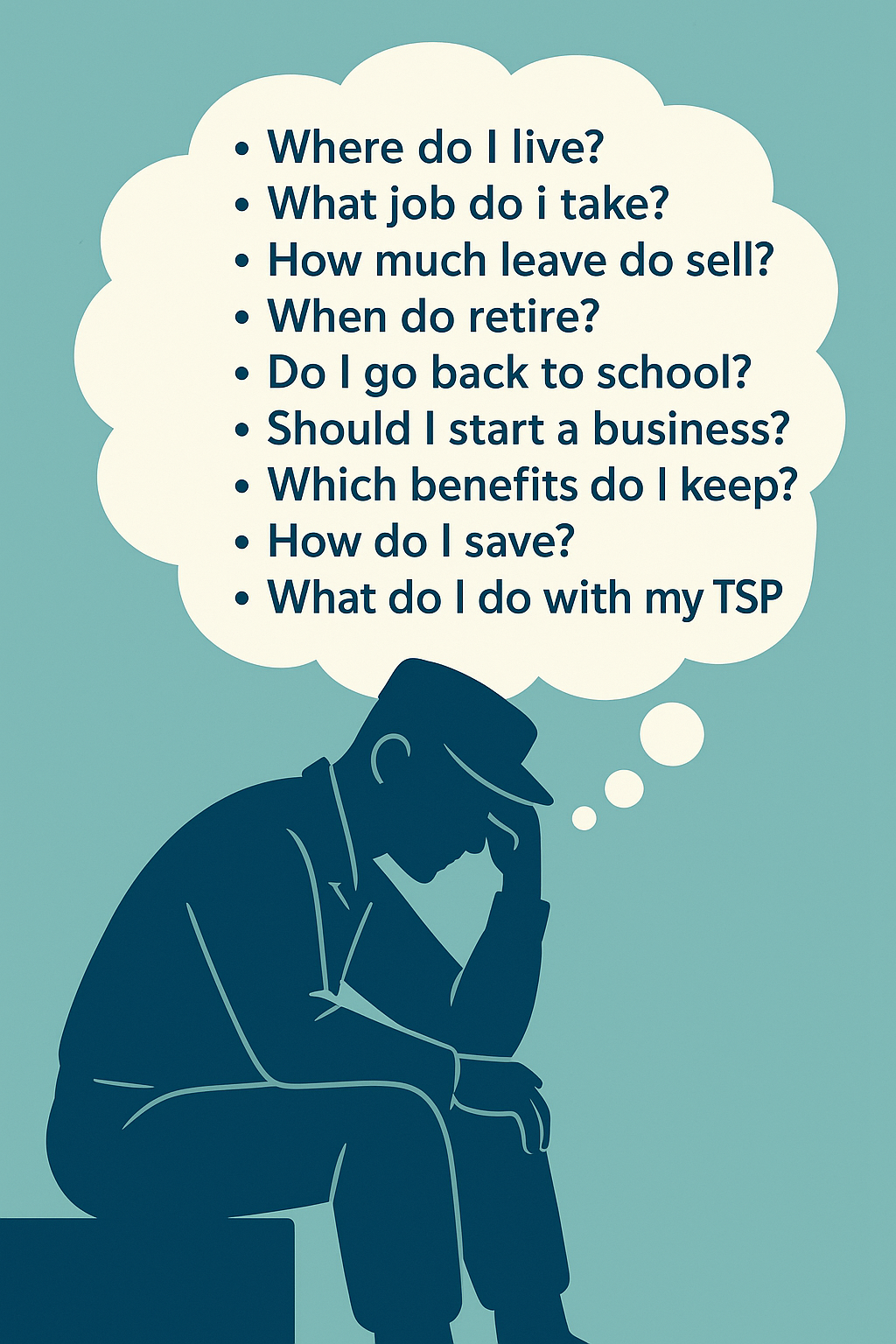

You’ve seen the world, but have you seen what’s truly possible for your life after the military? Too often, service members step straight into the next job without ever asking: What do I actually want? This article explores the silent momentum that pushes many retirees into high-paced second careers that mirror military life, without considering whether that’s the lifestyle they really want. If you’ve ever felt like you’re climbing a ladder just because it’s there, this is your invitation to pause, reflect, and choose with intention.

When we think about investing, risk is often the first word that comes to mind, and usually not in a good way. Risk is not something to fear, however. It is something to respect, acknowledge that it exists, and understand how we work with it.

As we reach the halfway point of the year, it’s an ideal time to pause and reassess your financial picture. Life moves fast—especially in military households—and it’s easy for your spending, saving, and goals to drift off course throughout the year without regular check-ins. A mid-year review is your opportunity to make small adjustments now that can have a meaningful impact by year’s end.