What Am I Paying For, Exactly? The Value of Initial Financial Advice

One of the most common questions prospective clients ask, either directly or indirectly, is a simple one: why does it cost so much to work with a financial advisor? Closely behind that is another question. What does a financial advisor actually do for their fee?

At the core, this is a question about value. Is the value of financial advice significant enough to justify the cost?

It is a fair question. It is also a difficult one to answer, which is exactly why it keeps coming up and why articles like this one continue to be written.

Why the Question Is So Hard to Answer

The challenge is that much of a financial advisor’s value is not easily quantifiable. Good advice is rarely a single, dramatic move. Instead, it is a series of small adjustments over time. Some are technical. Others are behavioral. All of them interact with unpredictable markets, evolving tax laws, and real life.

If the answer could be reduced to a clean equation, the conversation would be easy. Pay this fee, get that result. Unfortunately, it does not work that way. Advisors cannot promise specific dollar outcomes. Anyone who claims otherwise should raise immediate concerns.

Even so, the question deserves a thoughtful response.

This article is part one of a two-part series on how the value of financial advice is viewed in practice. Part one focuses on the early stages of the relationship: outreach, consultation, and onboarding. Part two addresses everything that follows.

There is an obvious bias here. It would be great if readers saw enough value to become clients. That said, this is far from the first time this topic has been explored. For another perspective, Christine Benz of Morningstar wrote a thoughtful piece titled Why I Have a Financial Planner.

Consultation: When Financial Pain Reaches the Breaking Point

When Personal Finances Become A Burden

There is a personal story that helps frame how many people approach financial advice.

During the final weeks of Officer Candidate School, there was persistent pain just below my kneecap. Anyone who has been through that environment knows the last place you want to end up is the medical office, where the risk of being dropped from training is very real. So I ignored the pain, completed OCS, and continued to feel pain below my knee.

It turns out that the diagnosis was a hairline fracture in the tibia.

The decision to “muscle through the pain” was not a proud moment, but at the time, the pain did not seem worth restarting the process all over again. Had I known the seriousness, I probably would have gone to medical sooner.

This same pattern shows up frequently in personal finances.

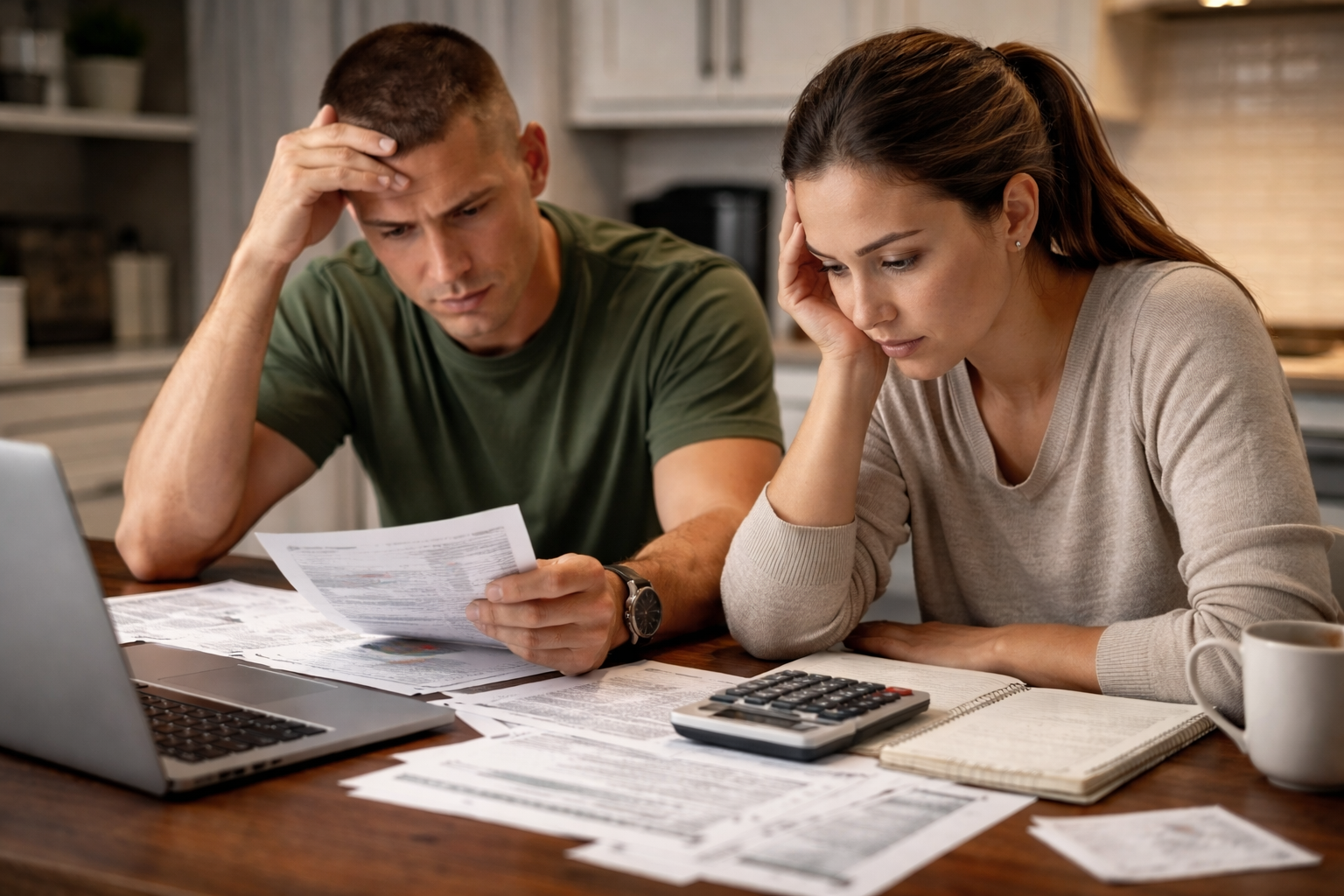

Many people wait far longer than they should before seeking help. The reasoning is understandable. Why pay someone for advice on topics that seem searchable online? Between articles, podcasts, and videos, it feels like everything should be solvable independently.

By the time someone reaches out, the pain has usually crossed into the "worth it - probably should have sought help earlier” category.

The Purpose of the First Conversation

Given it is a pain point that drives most prospective clients to schedule a consultation, the first objective is triage. That word can sound harsh, but it fits.

Sometimes the issues are technical. The debt feels overwhelming. The home decision feels paralyzing. The tax picture is unclear.

Other times the pain is more emotional. The income is strong, but the stress is crushing. Or there is simply a nagging sense that something should be done with money, even if it is not clear what that something is.

People express financial stress very differently. Some are stoic. Some cry. Some laugh. Some get angry.

Regardless of how it shows up, almost everyone wants the same things in that first meeting. They want to be heard. They want their problems to matter. And they want to know that solutions exist.

Listening Before Solving

The consultation is question-heavy by design. The goal is not to diagnose everything in one meeting, which would be impossible. The goal is to begin understanding both the symptoms and the underlying causes.

At a minimum, the consultation aims to do three things:

Actively listen and understand the situation being described.

Reinforce that help exists and that problems are solvable.

Provide something of value to walk away with, beyond generic reassurance.

This is not the meeting where tools come out or strategies are implemented. Roughly sixty to seventy percent of the time is spent understanding the person and their circumstances. The remaining time is spent explaining how the advisory relationship works.

When the meeting ends, there are important decisions on both sides.

The Fee Decision

For the prospective client, the decision is straightforward but not easy. Is this service worth the fee?

This is where fee tension lives. How do you assign a dollar amount to the relief that comes from knowing someone is capable of helping manage complexity? How do you price the feeling of safety or clarity?

The technical assumptions are usually understood. A licensed advisor can legally charge for advice. They can do the math. They understand the rules, the benefits, and the tax landscape.

What often becomes clear only after the meeting is the emotional shift. The sense that immediate pain can be addressed, and that long-term financial health can be improved. The value of that feeling is personal and subjective.

The Advisor’s Decision

There is also a decision on the professional side.

Not every advisor is the right fit for every situation. Some problems require specialization. While it is possible to learn many things, experience matters.

The longer someone works in finance, the clearer one truth becomes: the more you know, the more you realize how much you do not know.

This is why specialization exists. There are planners who focus on nurses, lawyers, truckers, and many other professions. The focus here is on military members and federal employees, because that is the space best understood.

Onboarding: Turning Conversation Into Structure

Once both sides agree that the relationship makes sense, onboarding begins.

Meeting One: Getting Organized

The goal of the first onboarding meeting is to understand the current financial picture.

This includes a walkthrough of the client portal, answering outstanding questions, and collecting the documents needed to build an accurate snapshot of finances as they exist today.

For some clients, this is simple. Documents are organized and readily available. For others, it is one of the most stressful parts of the process.

Often, clients are unsure what documents matter or where to find them. On top of that, financial information is deeply personal. Sharing it requires trust.

This meeting is approached with patience and care. Screen sharing is used to help locate documents, upload them securely, and reduce anxiety around the process. It can be a long meeting, and that is okay. Breaks are encouraged. If immediate opportunities or concerns are identified, they are addressed.

Between meetings, the information is reviewed and gaps are identified.

Meeting Two: The Strategic Vision Meeting

This meeting centers on values.

Many people feel stuck financially not because they earn too little, but because their money is not intentionally aligned with what matters most to them.

If travel is important, is there a plan to save for it? If family experiences matter, are resources being directed there? When was the last time spending was reviewed closely?

Charges that once felt reasonable often become unrecognizable over time.

This process helps identify the personal "why" behind money. Common values include time, travel, family, health, creativity, business ownership, and philanthropy.

For service members especially, this can be challenging. Years of structured schedules and expectations often leave little room to explore personal preferences. Identifying what does not matter is often just as valuable as identifying what does.

Values are not static. They evolve. This is not a one-time exercise, but an ongoing conversation.

Once values begin to take shape, actionable steps are developed. The starting point is almost always cash flow.

Income is reviewed, spending is categorized, and alignment with values is assessed. A common rule of thumb used is the 50-30-20 framework. No more than fifty percent toward mandatory expenses, thirty percent toward discretionary spending, and twenty percent toward financial priorities.

This is a guideline, not a law. However, experience shows that the further these categories drift out of balance, the more stress people feel about money.

Cash flow informs everything that follows. Education planning, retirement planning, emergency funds, insurance, investments, and tax planning all depend on it.

Meeting Three: Plan Review & Implementation

This is where ideas turn into action.

Gone are the days of dropping a massive printed financial plan on a desk. While there may be extensive data behind the recommendations, the focus here is clarity.

Visuals are used to show where things stand today and where they are headed. Goals are presented as flexible targets, not fixed endpoints, because life changes.

The first priority is addressing the original pain point that prompted outreach. From there, recommendations are placed in the context of the broader plan.

This meeting is not about complexity or showing expertise. It is about confidence. The goal is for clients to leave feeling that progress is possible and that the path forward is manageable.

Where the Value Sometimes Shows Up in Dollars

No financial advisor can guarantee specific outcomes, and anyone who claims otherwise deserves skepticism. But there are moments in financial planning work where the value is not just felt, it is visible. These are not guarantees or averages. They are real categories where meaningful corrections or improvements are discovered during the planning process.

Tax returns filed incorrectly. Military families move frequently, which creates complexity. State residency questions, combat zone exclusions, dual-income filing considerations. Errors on prior returns are not rare. Identifying and amending them can result in real refunds.

Investing at the wrong risk level. A TSP sitting at 100% G Fund for someone 20 years from retirement is is likely misaligned. Realigning investment risk with actual time horizon and goals is one of the most straightforward adjustments, and often one of the most impactful over time.

Cash flow that doesn't reflect priorities. Spending reviews routinely uncover subscriptions, automatic renewals, and habits that no longer serve the family. Redirecting even $200 to $300 per month toward savings or debt changes long-term outcomes significantly.

Tax planning that wasn't happening. Roth TSP vs. traditional TSP, Roth conversions in low-income years, combat zone tax exclusions. These decisions have long tails. Making the wrong call or no call at all has a cost.

Insurance gaps or over-coverage. Life insurance needs change. So does coverage through SGLI and dependent coverage. Families sometimes carry too little where it matters and too much where it doesn't.

Taken individually, any one of these discoveries might seem minor. But they have a way of compounding. A corrected tax return, combined with a cash flow redirect and a smarter TSP allocation, adds up quickly. In many cases, not all, but many, the corrections and improvements identified in the first year of the planning relationship meaningfully offset the cost of the fee itself. Sometimes they exceed it.

That is not a guarantee, and it is not the primary reason to engage a financial planner. The ongoing clarity, accountability, and guidance that follows is where the deeper value lives. But for those asking whether the fee is "worth it" in a tangible sense, the answer is often yes, and sometimes surprisingly so.

Onboarding Complete, But It’s Only the Beginning

This concludes part one of the series on the value of financial advice. Part two, What Am I Paying For, Exactly? The Value of Ongoing Financial Advice, focuses on what happens after onboarding.

The ultimate goal is to help service members and their families, and anyone considering working with a financial advisor, understand whether a values-based approach to financial planning is right for them. If you have any questions or comments, I’d love to hear from you at omen@4myndr.com.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Read the full disclosure.