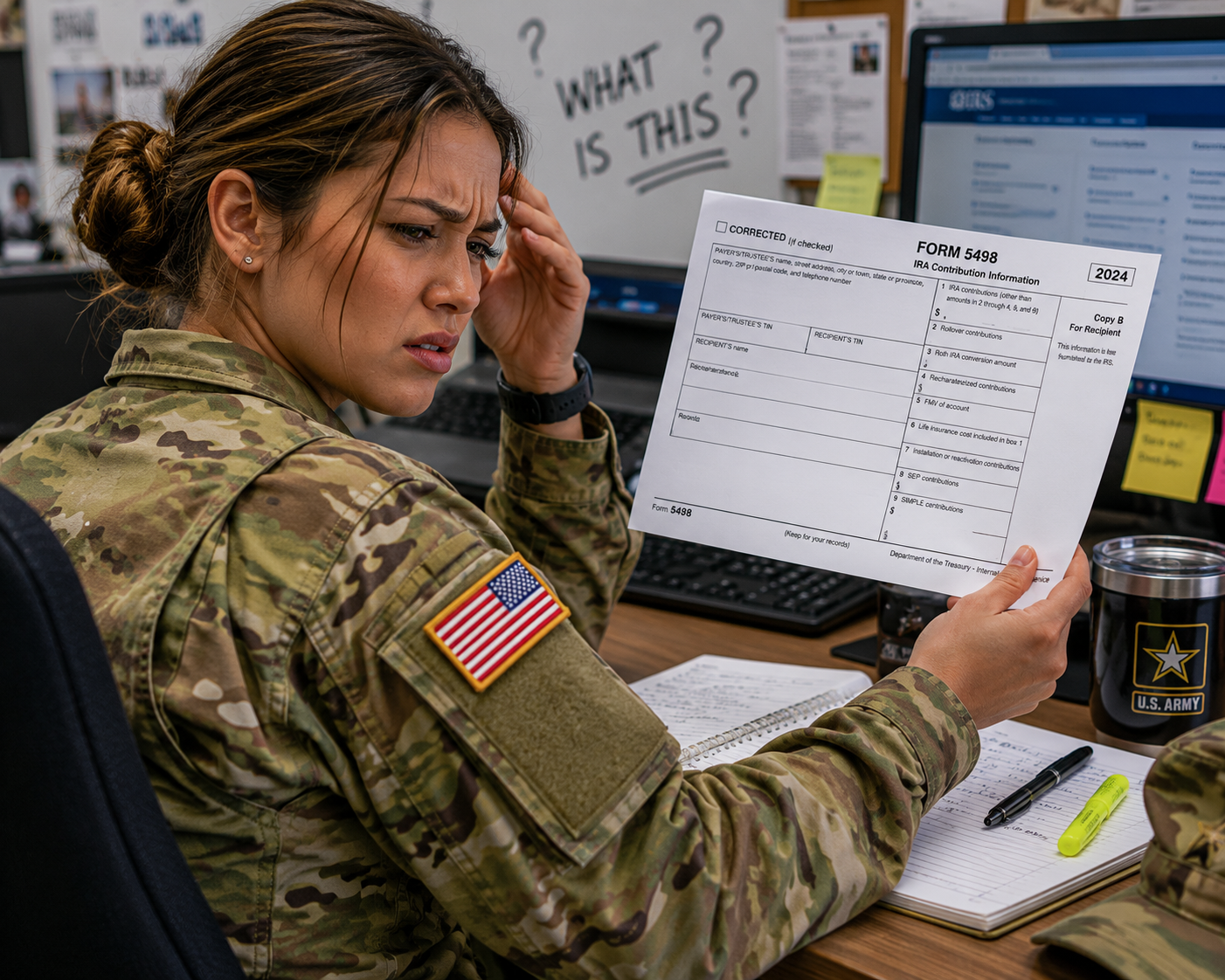

Got Form 5498 in the Mail? Here Is What It Means

Every May, a form arrives from an IRA custodian. Tax season is over, the return is filed, and now there is a piece of IRS paperwork sitting on the counter. That form is 5498, and despite the timing, nothing went wrong. But ignoring it has a way of creating expensive problems down the road.

The Supporting Fires of Personal Finance: Building the Right Financial Team for Military Life

In a combined arms operation, the mission succeeds not because one element outperforms the others, but because every element knows its role and coordinates toward a common objective. No single asset wins the engagement alone. The same principle applies to building a financial team for military life. The right professionals, working in their own lanes and communicating across them, give military families the structure to identify meaningful goals, aim their resources effectively, and execute a plan that holds together across every stage of service and beyond.

FEDVIP for Military Families: Dental and Vision Coverage Worth Understanding

TRICARE covers the medical side of military healthcare, but dental and vision are a different story. For military retirees and active-duty families, the Federal Employees Dental and Vision Insurance Program (FEDVIP) fills that gap with voluntary, competitively priced coverage. Understanding who qualifies, what it covers, and whether the premiums make sense for your family is worth a closer look before the next open season arrives.

TRICARE for Life and Medicare at 65: What Every Military Retiree Needs to Know

You spent decades earning your military retirement benefits. At 65, one of the most valuable pieces of that package clicks into place: TRICARE for Life alongside Medicare. But enrollment windows are unforgiving, the overseas rules surprise most retirees, and something called IRMAA can inflate your Medicare premiums for years if income is not planned carefully. Here is everything you need to know before that birthday arrives.

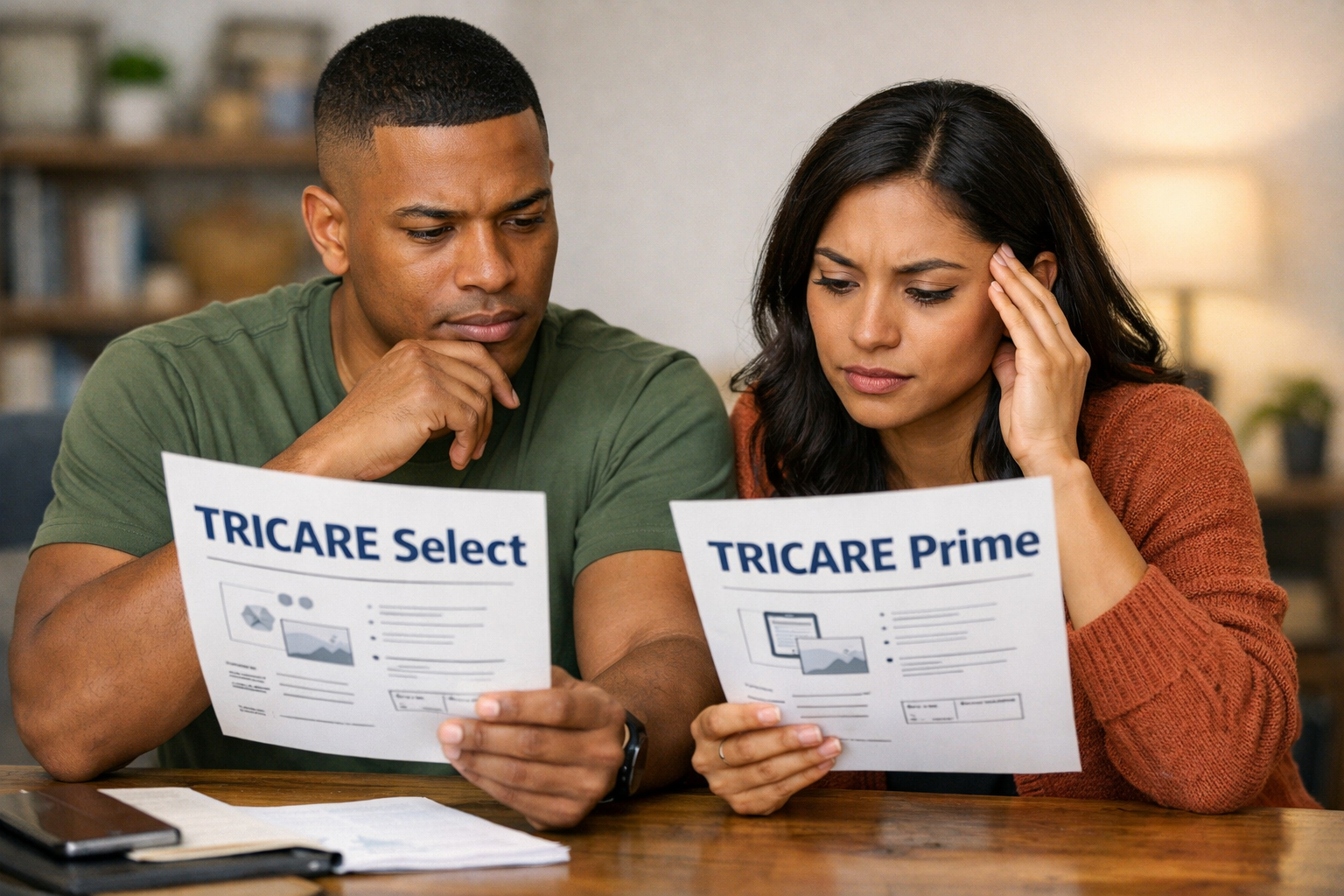

TRICARE Prime vs. Select: A Military Retiree’s Guide to Choosing the Right Plan

Comparing TRICARE Prime and TRICARE Select as a military retiree? This guide breaks down provider choice, enrollment fees, deductibles, copays, and catastrophic caps so you can make a confident decision for you and your family.

The 50-20-20-10: A Simple Cash Flow Framework for Military Families

The 50-20-20-10 rule of thumb offers a practical way for military families to think about cash flow. It helps create space for spending, saving, and giving while keeping mandatory expenses under control. More than anything, it serves as a conversation starter within households, helping couples stay aligned on financial priorities and avoid the stress that often comes when money begins to drift out of balance.

The Military Retirement Pension: How Guaranteed Income Can Change Your Investment Risk Strategy

Military retirement changes how investment risk should be evaluated. A military pension and VA disability income provide guaranteed, inflation-adjusted lifetime income that can significantly reduce reliance on an investment portfolio for mandatory expenses. This shift directly impacts asset allocation, retirement glide path decisions, and overall risk capacity. Unlike civilian retirees who depend heavily on 401(k) or IRA withdrawals, military retirees whose pension covers core living expenses may have greater flexibility to maintain higher equity exposure for long-term growth. Understanding your risk need, or how much your investments must generate to fund your lifestyle, is critical when designing a military retirement investment strategy.